Best Health Insurance Plans USA Costs and Coverage Guide

01-07-2026

Best health insurance plans USA are structured within the Affordable Care Act (ACA) Marketplace framework and categorized in standardized Medicare metal tiers Bronze, Silver, Gold, Platinum to balance the monthly premium expense against out-of-pocket medical liabilities. The best coverage is attained by determining requirements of managed care networks, such as Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO), household medical frequencies and zip code particulars associated in very pure methodology.

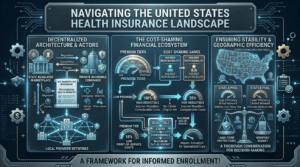

Navigating the United States Health Insurance Landscape

In the United States, the architecture of healthcare delivery is such that consumers must navigate a decentralized, multi-tiered marketplace to obtain medical coverage. In contrast with single-payer systems, choosing the best USA health insurance plans entails comprehending the clear-cut connections between state-regulated health marketplaces, private insurance companies and local healthcare provider networks. Under the Affordable Care Act (ACA) Marketplace, the national benchmark for individual and family coverage, benefit structures are standardized to identify ten essential health benefits that every qualifying plan must include: emergency services, maternity care, mental health treatment and prescription drug coverage.

But when people shop for low-cost health insurance plans they need to see beyond the sticker price on their premiums and instead explore the entire cost-sharing structure of the policy. A plan’s financial ecosystem is an intricate dance between deductibles, copayments, coinsurance rates, and maximum out-of-pocket limits. Low monthly premiums typically also go hand-in-hand with high annual deductibles, which means the insured is shouldered considerable financial responsibility before an insurance carrier ever starts to chip in on invoices for medical services. In contrast, premium-tier plans dramatically decrease point-of-service costs and can fill the void with insurance coverage for individuals needing frequent specialized medical care.

It ensures stability of access to health care over a policy year to help prevent unanticipated medical debt from occurring as a result of poor or unpredictable designs and structural trade-offs. Since in the U.S. insurance risk pools are based on state and rating area, financial efficiency and network coverage can differ greatly geographically. With that said, a thorough consideration should balance both the long-term contractual protections of a plan against the short-term limitations of a household’s monthly operating budget.

Actuarial Metal Tiers: Finding a Middle Ground

The ACA Marketplace sorts insurance designs into four unique metallic shapes characterized by their portion of expected healthcare expenses paid for or secured out of your pocket. Actuarial Value This is the proportion of total average medical costs that a plan will pay for a standard population (the other portion being paid by the consumer).

Low-Premium, High-Deductible Configurations

These use low relative premiums and high deductibles in order to serve as a form of catastrophic financial protection for those who have typically not used a small amount of clinical access (i.e., their healthcare utilization profiles) during the cost-effectiveness experiment that is this policy configuration.

Bronze Tier/ Framework:

- Bronze plans have the lowest monthly operating expenses and cover around 60 percent of costs on an actuarial basis. The most significant trade-off is a higher annual deductible, which often obligates individuals to spend thousands of dollars on non-preventive medical attention out of pocket before any cost-sharing features are triggered.

Silver Tier Benchmarks:

- Silver is the structural median with an actuarial value of around 70 percent. This particular tier is the starting point for determining federal premium subsidies and is also the only route through which cost-sharing reductions are delivered, effectively lowering deductibles and copays for qualifying lower-income households.

High-Premium, Low-Deductible Foundations

Foundations of high-premium, low-deductible plans target overall families in charge for unending medicine conditions that are predictable by prescriptions or planned operation intercessions.

Gold Tier Architectures:

- The Gold plans have a high actuarial value (80 percent), absorbing the majority of treatment costs at the cost of higher, more predictable monthly premium commitments. Minimizing point-of-service frictions is key to the efficacy of this tier, especially for those who consult specialists often.

Platinum Tier Standards:

- Platinum plans provide the richest level of coverage (90 percent actuarial value). They have effectively no or extremely low deductibles the insurance company takes on nearly full financial responsibility after clinical services as soon as the policy cycle resets.

The architecture of Private Health Care Insurance: The HMO And Other Managed Care Networks (PPO & EPO Plans)

What makes best health insurance plans USA work very well depends on the Managed Care Network Delivery Model. What a patient can access beyond the list of pre-approved doctors and whether administrative approval in seeking referred intervention from specialists outside that list is determined by the network structure.

Health Maintenance Organization (HMOs):

HMOs implement a very narrow and local network model that is focused on controlling costs and sending all care through a central point of coordination. You will be required to assign a Primary Care Physician (PCP), the institutional gatekeeper of the patient’s healthcare universe. All visits to a specialist (such as a dermatologist or cardiologist) after that require a direct referral from the PCP. Finally, the HMO contracts promise not to pay anything for out-of-network services (as long as the patient is still alive) and the insurer has virtually no liability from unauthorized bills.

Preferred Provider Organizations (PPOs):

In stark contrast to HMO constraints, PPOs offer the maximum amount of clinical flexibility and open-access care pathways. PPOs do not require policy holders to choose a Primary Care Physician and do not require formal referrals for visiting specialty medical care practitioners. The network model has two separate cost schedules an in-network price backed by heavy negotiated discounts and an out-of-network payment which lets patients see any licensed physician in the nation. PPOs appeal to active families or those who just want the very best specialists, as care that is out of network typically comes with yet higher deductibles and coinsurance percentages but offers structural freedom.

Exclusive Provider Organizations (EPOs):

EPOs are a relatively new hybrid delivery system that combine the network boundaries of an HMO with the operational flexibility of a PPO model. An EPO plan, similar to an HMO, provides no coverage in the out-of-network setting, making patients solely reliant on the provider panel designated by their carrier. An EPO also removes the primary care gatekeeper mechanism but substitutes the provider access restrictions for direct access to a specialist without having to follow stricter referral practices – mitigating long wait times and premium costs like a PPO.

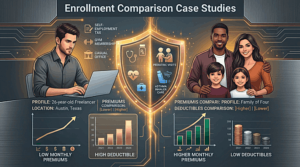

Contextual Application: Case studies around enrollment comparison

By looking at real enrollment examples, it shows you a way that measuring metrics of health insurance quotes USA helps different demographics optimize their coverage by risk and how much they can afford.

Case A: Young Man Servicing Cheap Goods

Austin, Texas: Aged 26 Freelance Digital Consultant since graduating from college this year, only semi-annual preventative screeners and seasonal generic prescriptions with low cost best health insurance plans USA, she examines multiple options on her state’s insurance exchange. She chooses a bronze HMO plan with $50 monthly premiums (after subsidies) along with a $7,500 annual deductible because she has low utilization of medical services.

Since federal law requires zero out-of-pocket costs for her annual physical and preventive blood panels, those evaluation studies during the policy year come in at 100%. When she has an unexpected episode of acute strep throat, she goes to the plan’s integrated telemedicine portal and gets a prescription from someone in network for a flat $25 copay. Low-premium legacy allows her capital preservation AND absolute financial ceiling against catastrophic health crisis.

Scenario B: Full Family Allocation Plan

Chicago, Illinois: A family of four requires comprehensive care parameters recorded for each family member, such as routine pediatric visits, speech therapy sessions and maintenance medications prescribed for asthma control. Out of control out-of-pocket spikes and volatile USA health care costs have a significant effect on household finances; therefore, the family examines available options via the free are-to-all health insurance quotes USA service to protect their household budget from sudden expense crises.

Their choice is a Silver PPO that has an elevated $450 premium per month, but also offers a lower $3,000 family deductible and capped $20 copays for trips to the specialist. The parents can keep going to their long-time pediatrician without having to establish a referral pipeline, since the plan is offered with an open PPO network. The predictable copays guarantee these weekly therapy sessions and monthly inhaler refills never reach the primary deductible, so this household can pay for their healthcare needs with strong statistical precision.

People Also Ask (PAA)

What is a health insurance premium and what is a deductible?

Health insurance premiums are the fixed monthly dollars that you pay to your carrier at a regular periodic basis (once every month) in order to sustain an active policy. A deductible is a specified dollar amount that you pay out of pocket for medical services before your plan begins paying to cover any health care.

What are ACA premium tax credits and how do they help lower the cost of health insurance?

ACA premium tax credits are direct subsidies from the federal government that reduce your monthly health insurance premiums on a sliding scale, adjusted for estimated household income. Once applied, these tax credits go directly to your insurer of choice, lowering the total amount due each month.

Can you get a health insurance plan outside of the annual Open Enrollment Period?

Outside the standard Open Enrollment Period, you may only buy a health insurance plan when you have a Qualifying Life Event that entitles you to a Special Enrollment Period. Your bumps in the road are big changes, like tying the knot, having a baby, losing your job-based insurance or moving somewhere else for good (hello new zip code).

Maximum Out-of-Pocket Limit in best health insurance plans USA?

The maximum out-of-pocket limit is the total amount you will ever pay for covered medical services in a calendar year. When the total amount you pay in deductibles, copayments, and coinsurance payments reaches a specified limit called your out-of-pocket maximum for that year, the insurance carrier pays 100 percent of all other eligible medical expenses after completing this maximum.

What do some health insurance plans only offer NO out-of-network doctors at all?

By limiting access to out-of-network providers HMOs and EPOs keep costs low while ensuring that all in-network doctors follow the same quality standards. They may even limit coverage to a subset of so-called “networks” of providers who agree to accept lower rates, which allows insurance companies to charge their policyholders lower monthly premiums.

Editorial Review & Author Information

Written & reviewed by Pablo Pérez This article was written and reviewed by Pablo Pérez, a licensed best health insurance plans USA advisor and co-founder of RGP Agency. The content is based on practical experience helping individuals and families navigate the ACA Marketplace, compare metal-tier plans (Bronze, Silver, Gold, Platinum), and choose the right managed care network HMO, PPO, or EPO based on household medical needs and budget.

RGP Agency is a Texas-based insurance agency specializing in affordable family health insurance plans, including affordable care act health insurance coverage, health insurance with dental and vision plans, critical illness health insurance coverage, and indemnity plan options. The agency focuses on helping individuals and families understand their coverage options, compare premiums and deductibles, and select a plan that balances monthly costs with long-term financial protection.

Corporate Verification & Contact Information

For plan comparisons, enrollment guidance, or health insurance quotes, you may contact the official office below:

Office Address: 8376 Davis Blvd, Suite 246, North Richland Hills, TX 76182

Direct Phone: (817) 973-5255

Official Website: rgpagency.com

Authority Citations

RGP Agency Editorial Team. (2026). Affordable Family Health Insurance Plans & ACA Marketplace Guide. RGP Agency Health Insurance Series. https://rgpagency.com/health-insurance/

References & Authoritative Sources

Below is a curated reference section to support the concepts explained in this article. These sources are widely recognized in the health insurance and consumer education space, commonly used for ACA plan definitions, metal-tier structures, and managed care network rules.

- HealthCare.gov Official U.S. government site for ACA Marketplace plans, enrollment periods, and subsidy information.

- CMS.gov Centers for Medicare & Medicaid Services, federal source for ACA regulations, essential health benefits, and metal-tier actuarial value standards.

- KFF.org Kaiser Family Foundation, independent health policy research on premiums, deductibles, and marketplace trends.

Social Share

Life Insurance

Protect your family’s future.

Health Insurance

Stay healthy, stay protected.

Income Annuities

Turn savings into steady income.