Cash Value Life Insurance Calculator and Policy Value

01-07-2026

A cash value life insurance calculator determines how the money grows over the years in a cash value life insurance by looking at premiums, interest, dividends and fees associated with your plan. It assists you in forecasting the cash surrender value of the policy as well as the long-term financial growth within permanent life insurance structures.

A term life insurance calculator is a tool used to assess the savings-type value of a permanent life insurance policy while still providing a death benefit. Unlike term coverage, it integrates whole life insurance protection with investing, which means that this kind of insurance coverage product can be a dual-purpose economic tool for extensive-term setting up. If you are analyzing plans, reviewing a term life insurance rates by age chart can help clarify how costs scale over time.

This calculator is important for policyholders to know how payments in the form of premiums become cash value that future buyers will have access to. It enables you to bring different facets of policy structures precisely its premiums, benefits or cash flows on par while utilizing the surrender value and finding a whole life/other plan that fits your financial goals.

How Cash Value Life Insurance Works

Cash value life insurance is a type of permanent life and health insurance that builds up the cash value over time, along with a death benefit. That cash value appears along with the death benefit (the amount payable at the time of death) in an eligible permanent life policy and grows tax-deferred, typically to be accessed during the lifetime of the insured via loans/withdrawals or full surrenders.

The structure of the concept involves arriving at three components from each premium due cost of insurance, administrative unit and a bucket for cash accumulation. The accumulation part is the one that makes internal value in the policy money. This, over time, builds up a cash reserve to be used against emergencies, supplementing retirement income or large expenditures.

Types of conventional cash value policies include:

Whole life insurance

Universal life insurance

Variable life insurance

There are different crediting types, but the main idea behind all three types is long-term internal accumulation in a life insurance contract.

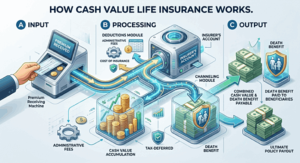

Working Mechanism of a Cash Value Life Insurance Calculator

A cash value life insurance calculator predicts the future worth of your policy by crunching various financial variables. This will normally consist of your age, the amount of premium you pay, the type of coverage (preferably a small whole life policy), and your expected duration of coverage along with interest rate assumptions.

The calculator simulates cash value growth over the years using compound interest mechanics and the unique crediting formulas of insurers. For instance: whole life policies typically use a fixed growth rate, while universal life policies rely on changing interest rates.

Key inputs used in calculation:

Annual or monthly premium amount

Policy duration (years in force)

Assumed interest or dividend rate

Cost of insurance deductions

Policy fees and charges

The output generally includes projected:

Cash surrender value

Accumulated cash value over time

Death benefit projections

The point of breakeven (where cash value accumulates beyond total premiums due) This enables policyholders to visualize long-term scenarios before agreeing on or altering a policy.

What is the cash value and what is the cash surrender value of life insurance

The cash value of life insurance is the entire amount of savings you have built up inside your policy. It has full account balance (internal to you) before applying any of the penalties or making deductions.

Life insurance The cash surrender value of life insurance is the actual amount the policyholder receives when canceling a policy. This worth is commonly lower than whole cash worth as a result of give up fees, excellent loans, or early termination penalties.

Both are important in their relationship with each other:

Cash Value = Total internal funds accumulated

Cash Surrender Value = Amount one can take out after deductions

In time, surrender charges tend to go down, hence the distance between cash value and surrender value is getting smaller. For later policy years, the two values very often almost exactly coincide.

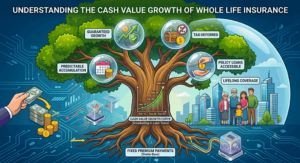

Understanding the Cash Value Growth of Whole Life Insurance

Whole life insurance is the most structured method for building cash value. This one guarantee growth of your investment based on the whole life insurance cost defined by the insurance provider. This renders it both predictable and stable as opposed to market-linked policies.

Usually this grows slowly but snowballs in later years. Initial premiums comprise a much larger proportion of insurance costs, whilst latter premiums contribute more towards cash value growth.

Whole Life Cash Value Key Features:

Guaranteed minimum growth rate

Fixed premium payments throughout life

Predictable long-term accumulation curve

Policies which allow loans against cash value

This is especially helpful for estate planning strategies and conservative finance approaches.

Purchasing Life Insurance As A Financial Asset (Cash Value)

Cash value life insurance provides protection and is also an asset. Unlike a term insurance policy, it does not have an expiry after a specific time period and can continue to acquire home equity as long as premiums are paid.

The cash value is often used strategically by policyholders:

Emergency liquidity through policy loans

Supplementary retirement income

Funding education or large expenses

Tax-advantaged wealth transfer planning

But if the loan is not repaid it decreases both future growth and death benefit against the policy. This makes disciplined financial management critical.

From a financial planning perspective, it has characteristics of an insurance plan, a savings event and long-term investment packaged together into one contract.

Cash Value Life Insurance — What Is It in Real Life

Realistically it is a long-term contract to have some of your premium donate savings that you can access through life insurance plans. The longer the policy remains in force, the more it is worth it.

Whereas with a taxable savings account, growth is taxed annually, with an IUL you have tax-deferred growth. Provided that you do not withdraw excess values from the insurance policy, withdrawals and/or policy loans are generally tax-free, but they can be structured in such a way to have some sort of tax impact.

The main trade-off is cost vs flexibility it seems to be:

Premiums Are Higher Than Term Life

Lower initial liquidity in early period

Long-term cash accumulation benefits

Lifelong coverage protection

It, therefore, lends itself to people who have steady income with long-term financial planning objectives from a trusted provider like RGP Agency.

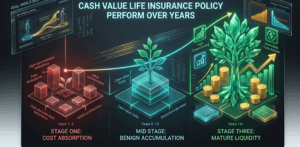

Cash Value Life Insurance Policy Perform Over Years

Traditional cash value life insurance policies have a relatively consistent lifecycle. Since more goes into insurance and administrative deductions in earlier years, cash value increases slowly at first. The policy starts to grow and accumulates rapidly.

We can think of the performance curve as three separate stages:

Stage One (Year 1 through Year 5): Minimal cash value growth, maximum cost absorption

Mid Stage (Years 5–15): Gradual benign trend, value becomes apparent

Stage 3: Mature (15+ years): High compounding, increased access to liquidity

Results are highly dependent on consistency of premiums and crediting performance of the insurer. As long as your payments are uninterrupted, without interruptions over the 40 years of accumulation you will accumulate more and poorer.

How Cash Value Calculations Work in the Real World

Cash value calculators allow financial planners to model performance over a long period of time and are commonly used in various planning scenarios. They allow people to see how a policy can relate and assist in retirement planning, estate structuring, and emergency funding plans.

Common real-world uses include:

Modeling income in retirement with policy loans

Comparison of the whole life vs term life insurance configuration costs

Assessing the benefit in surrendering early as opposed to holding on for extended periods

Estate planning for effective asset transfer

So, for instance, we asked if a policyholder paid the same premiums every year for the next 20 years, is there enough cash value now to replace other investments that are critical to income in retirement.

Such long-term projections would reduce uncertainty and improve financial decision-making.

People Also Ask (PAA)

What to Use a Cash Value Life Insurance Calculator For?

It is used to estimate the cash value a life insurance policy will accumulate over time due to premiums, interest rates and structure of the policy.

How does the cash value in life insurance gain?

Cash value is accumulated through interest credits (the crediting rate) and, in some policies, through dividends along with the allocation of a portion of premium payments less insurance costs and fees.

Can I extract cash value from life insurance?

Policyholders can access cash value but this reduces the death benefit and limits long term compound growth.

What is the difference between cash value and surrender value?

Cash value is the total amount in the policy and surrender value is after costs of startup fees or penalties from cancelling.

Types of cash value life insurance You’re comparing quotes and life insurance types, but getting confused about what you shop for?

It depends on financial goals. It is best for long-term planning as far as the need for wealth accumulation or permanent coverage and not actually short-term savings.

Editorial Review & Author Information

Written & Reviewed By: Pablo Pérez This article was written and reviewed by Pablo Pérez, a financial advisor and co-founder of RGP Agency. The content is based on practical experience in cash value life insurance planning, permanent life insurance structures, and long-term policy value strategies.

RGP Agency is a Texas-based financial services organization specializing in cash value life insurance, wealth protection, and long-term financial planning solutions. The agency focuses on helping individuals and families understand how permanent life insurance can be structured for cash accumulation, legacy planning, and policy efficiency.

Corporate Verification & Contact Information For policy-related inquiries, cash value illustrations, or life insurance planning services, you may contact the official office below:

· Office Address: 8376 Davis Blvd, Suite 246, North Richland Hills, TX 76182

· Direct Phone: (817) 973-5255

· Official Website: rgpagency.com

References & Authority Citations

RGP Agency Editorial Team. (2026). Cash Value Life Insurance Policy Structure & Long-Term Value Planning. RGP Agency Financial Planning Series. https://rgpagency.com/life-insurance

References & Sources

Below is a carefully curated reference section to support the concepts explained in the article. These sources are widely recognized in the insurance and financial education space and are commonly used for policy definitions, tax treatment, and cash value mechanics.

Insurance Education & Policy Fundamentals

- Investopedia – Cash Value Life Insurance Guide

Provides a detailed breakdown of how cash value life insurance works, including accumulation structure, policy types, and key financial mechanics. - NAIC – Life Insurance Consumer Resources

Explains regulatory standards, consumer protections, and general life insurance policy structures across the U.S.

Cash Value, Loans & Surrender Value Explanation

- Policygenius – Cash Value Life Insurance Explained

Covers how cash value grows, how policy loans work, and the difference between cash value and surrender value. - Forbes Advisor – Whole Life Insurance Overview

Explains whole life insurance structure, guaranteed growth, and long-term financial implications.

Tax Treatment & Financial Rules

- IRS – Life Insurance & Tax Guidelines

Official tax authority guidance explaining how life insurance proceeds, loans, and withdrawals are treated under U.S. tax law.

Policy Comparison & Financial Planning Insights

- The Balance – Types of Life Insurance Policies

Breaks down term vs permanent life insurance, including cash value accumulation differences.

Bankrate – Cash Value Life Insurance Explained

Provides real-world financial perspective on when cash value policies make sense and how calculators estimate long-term growth.

Social Share

Life Insurance

Protect your family’s future.

Health Insurance

Stay healthy, stay protected.

Income Annuities

Turn savings into steady income.