How Much Is Final Expense Life Insurance?

02-07-2026

Final expense life insurance costs typically range between $30 and $70 per month for $10,000 of permanent whole life coverage, depending on the applicant’s exact age, biological gender, and tobacco usage. Highly structured policies for older seniors or those seeking guaranteed issue final expense life insurance with no medical questions can scale from $80 to over $150 monthly as underwriting risks increase.

Understanding Final Expense Life Insurance Costs

Evaluating life insurance for final expenses requires analyzing how insurance carriers calculate premium rates for permanent small-face whole life policies. Final expense life insurance, often structurally referred to as burial insurance or funeral insurance, features simplified underwriting designed specifically to cover end-of-life costs, such as standard funeral services, cremation, remaining medical debt, and legal fees. Unlike traditional term life insurance policies that expire after a set period, a final expense policy is permanent, meaning the death benefit remains guaranteed for the lifetime of the policyholder, provided monthly premiums are paid consistently.

The baseline final expense life insurance cost is highly dependent on the entry age of the insured individual, meaning that every year an applicant delays enrollment, the fixed premium obligation permanently climbs. For instance, a healthy, non-smoking 50-year-old female can secure a $10,000 policy for approximately $24 to $30 per month, whereas a 70-year-old female purchasing the identical policy face value will see final expense life insurance rates reach roughly $53 to $64 per month. Actuarial projections prioritize life expectancy metrics, which directly explains why biological males pay higher premiums across all age tiers relative to their female counterparts.

A primary functional advantage of this asset class is the ironclad predictability of the financial structure. Once an insurance company approves a policy application, the monthly premium rate locks in permanently and can never increase, regardless of subsequent age milestones or declining physical health conditions. Concurrently, the total face value or death benefit remains completely fixed, ensuring that the legacy funds designated for beneficiaries do not diminish over time.

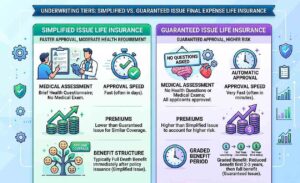

Underwriting Tiers: Simplified vs. Guaranteed Issue Final Expense Life Insurance

The path chosen during the application process determines the baseline rate structure and the operational mechanics of the death benefit payout. Carriers divide final expense life insurance into two primary operational underwriting categories: simplified issue and guaranteed issue.

Simplified Issue Final Expense Coverage

Simplified issue policies represent the standard entry point for senior consumers who possess relatively stable health histories. This category delivers final expense life insurance no exam benefits, meaning applicants avoid invasive physical checks, blood draws, or urine samples. Instead, underwriters rely entirely on a basic digital questionnaire regarding historical medical diagnoses, automated prescription drug history database checks, and Medical Bureau reviews.

Because the insurance company gathers verifiable health data via these digital lookbacks, they can accurately segment risk profiles. Consequently, simplified issue policies yield the best final expense insurance rates in the marketplace. These policies grant immediate day-one coverage, meaning the entire death benefit is payable to the designated beneficiaries even if the policyholder passes away only a single month after policy inception.

Guaranteed Issue Final Expense Coverage

Guaranteed final expense life insurance addresses the coverage needs of individuals with severe pre-existing chronic conditions, cognitive impairments, or terminal illnesses. This financial vehicle features final expense life insurance no medical questions parameters, preventing an insurance company from denying coverage based on physical health status, historical hospitalizations, or pharmaceutical use.

Because carriers accept total, unmitigated health risks blindly, they adjust their corporate risk exposure through two specific financial mechanisms:

Elevated Premium Pricing:

Policyholders pay significantly higher monthly rates per thousand dollars of coverage compared to simplified issue alternatives.

Graded Death Benefit Provision:

Policies include a strict two-year waiting period; if the insured dies from natural causes during the first 24 months, beneficiaries receive only a refund of paid premiums plus a small interest percentage (typically 10%), rather than the full face value.

Core Variables Impacting Monthly Premium Structures

Analyzing the direct components that control final expense life insurance rates reveals why seemingly identical face amounts can deviate significantly in monthly market cost. Insurance actuarial tables compress multiple external vectors to calculate exact policy costs.

Age at Application Inception:

Age remains the absolute dominant predictor of premium cost. To understand how numbers scale over time, looking at a term life insurance rates by age chart shows how rates step up systematically with each birthday.

Biological Gender Assignment:

Statistically documented mortality differences show women outliving men by several years, allowing carriers to lower baseline female rates.

Tobacco Consumption Habits:

Nicotine consumption significantly degrades systemic health, leading carriers to assess a 30% to 100% premium surcharge on active smokers.

Selected Death Benefit Capitalization:

Face values scale proportionally, making a $25,000 policy cost exactly five times more than a baseline $5,000 policy under identical demographic underwriting.

Real-World Application: Final Expense Policy Implementation

Analyzing actual scenario applications clarifies how distinct consumer groups structure their final expense life insurance coverage to protect surviving family members from sudden financial burdens.

Scenario A: Standard Simplified Issue Implementation

A 62-year-old non-smoking male manages mild, controlled hypertension through basic, low-tier prescription medication but otherwise maintains clean medical markers. Seeking to shield his children from paying out-of-pocket for a standard traditional funeral and burial, he applies for a simplified issue policy with a permanent face value of $15,000.

Because his medical history contains no disqualifying cardiovascular incidents, the digital underwriting system approves him for immediate, first-day full coverage. The carrier establishes a fixed monthly premium of approximately $65, a rate that remains immutable for the remainder of his life.

Scenario B: Guaranteed Issue Implementation

A 68-year-old female smoker seeks protection but has suffered a stroke within the past year and manages diagnosed type 2 diabetes with severe peripheral neuropathy. Due to recent major cardiovascular events, standard simplified underwriting channels instantly disqualify her from day-one coverage platforms.

To secure financial protection, she shifts her strategy to a guaranteed issue life insurance policy with no medical questions, selecting a target death benefit of $10,000. The carrier approves the application automatically without viewing her medical charts, setting a fixed permanent rate of approximately $80 per month subject to a mandatory 24-month graded waiting period clause handled by RGP Agency.

People Also Ask (PAA)

What is the average cost of a $10,000 final expense life insurance policy?

A $10,000 final expense insurance policy costs an average of $30 to $50 per month for individuals in their 50s and 60s. For applicants entering their 70s or 80s, the monthly cost typically increases to between $70 and $130, depending heavily on gender and tobacco use.

Can you obtain final expense life insurance with zero medical questions?

Yes, guaranteed issue final expense life insurance allows individuals to secure coverage completely free of health questionnaires, physical examinations, or medical record lookbacks. These life insurance policies ensure automatic approval for any applicant meeting basic age requirements, usually ranging from 50 to 80 years old.

How does tobacco use affect final expense life insurance rates?

Tobacco use triggers substantial rate increases, often doubling the monthly premium cost compared to non-smoking applicants within the same age and gender brackets. To qualify for standard non-tobacco rates, most life and health insurance companies require the applicant to be completely nicotine-free for a continuous 12-month period.

What happens if the insured individual passes away during the two-year graded period?

If the insured passes away from natural causes during the initial two-year waiting period of a guaranteed issue policy, the carrier does not pay out the full face value death benefit. Instead, the company issues a full refund of all monthly premiums paid up to that date, plus an additional statutory interest payout, typically fixed at 10%.

Are the death benefit payouts from final expense insurance policies taxable?

The death benefit payout from a final expense life insurance policy is distributed to designated beneficiaries completely free of federal income tax. The funds are delivered as a lump-sum cash payment, allowing beneficiaries full discretion to pay for funeral expenses, clear remaining medical debts, or resolve outstanding household bills.

Editorial Review & Author Information

Written & Reviewed By: Pablo Pérez

This article was written and reviewed by Pablo Pérez, a financial advisor and co-founder of RGP Agency. The content is based on practical experience in permanent small-face whole life structures, simplified senior underwriting, and estate-clearing final expense strategies.

RGP Agency is a Texas-based financial services organization specializing in final expense life insurance, wealth protection, and legacy planning solutions. The agency focuses on helping individuals, seniors, and families understand how permanent protection can be structured with locked-in premiums to cover end-of-life expenses and eliminate sudden financial burdens.

Corporate Verification & Contact Information

For policy-related inquiries, final expense rate illustrations, or senior life insurance planning services, you may contact the official office below:

- Office Address: 8376 Davis Blvd, Suite 246, North Richland Hills, TX 76182

- Direct Phone: (817) 973-5255

- Official Website: rgpagency.com

Authority Citations

RGP Agency Editorial Team. (2026). Final Expense Policy Mechanics & Simplified Underwriting Frameworks. RGP Agency Senior Protection Series. https://rgpagency.com/life-insurance/final-expense-insurance/

References & Authoritative Sources

Below is a carefully curated reference section to support the concepts explained in the article. These sources are widely recognized in the senior insurance and consumer financial education space and are commonly used for simplified policy definitions, tax treatment, and graded death benefit rules.

- RGP Agency Final Expense Directory: Official specialized portal detailing senior burial coverage tiers, no-exam policy qualifications, and permanent rate tables.

- RGP Agency Core Protection Overview: Broad operational framework analyzing permanent small-face whole life policies against alternative traditional options.

- Investopedia – Burial Insurance Guide: Explains the fundamental structure of final expense insurance, including simplified underwriting and the handling of immediate end-of-life costs.

- NAIC – Life Insurance Consumer Resources: National Association of Insurance Commissioners portal detailing state regulatory standards for two-year graded periods and senior consumer protections.

- Policygenius – Final Expense Insurance Explained: Breaks down exact premium differences between simplified issue and guaranteed issue parameters for older demographics.

- Forbes Advisor – Senior Life Insurance Cost Breakdown: Analyzes how age, biological gender, and nicotine use systematically impact long-term actuarial tables and monthly rates.

- IRS – Life Insurance Proceeds & Tax Treatment: Official federal guidance confirming tax-free lump-sum status for permanent life insurance death benefit distributions to beneficiaries

Social Share

Life Insurance

Protect your family’s future.

Health Insurance

Stay healthy, stay protected.

Income Annuities

Turn savings into steady income.