MYGA vs Fixed Indexed Annuities: Which Is Better?

15-07-2026

You spent thirty years building a nest egg. One bad market year shouldn’t decide how the next thirty go. That’s the real reason so many retirees end up comparing MYGA vs fixed indexed annuities, two products that both promise safety, but get there in completely different ways. Even the longer version, what is MYGA annuity coverage really protecting, comes down to one simple idea once you strip the jargon away. Stick with me here and you’ll walk away knowing exactly which one fits your retirement, not just the textbook version of both.

You spent thirty years building a nest egg. One bad market year shouldn’t decide how the next thirty go. That’s the real reason so many retirees end up comparing MYGA vs fixed indexed annuities, two products that both promise safety, but get there in completely different ways. Even the longer version, what is MYGA annuity coverage really protecting, comes down to one simple idea once you strip the jargon away. Stick with me here and you’ll walk away knowing exactly which one fits your retirement, not just the textbook version of both.

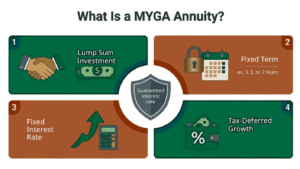

What Is a MYGA Annuity?

Not catchy, but accurate. You hand an insurance company a lump sum, they hand you back a fixed rate of interest for a set number of years, usually somewhere between three and seven. No market ups, no market downs, just a number you agreed on at the start and a number you get at the end.

People ask what a MYGA annuity actually does for them in practical terms, and the honest answer is: it removes a decision. Once it’s locked in, you’re not checking the news every morning wondering how your retirement savings did overnight. A multi-year guaranteed annuity is closer to a CD than a stock, just with better rates most years and tax-deferred growth tucked in as a bonus. If you’ve ever wondered what MYGA annuity protection is worth, that peace of mind is most of it.

How MYGA Rates Work Today

Here’s the part nobody loves hearing: MYGA rates aren’t fixed forever, only fixed for your contract. The rate available today might not be there next quarter. So if you’re sitting on cash waiting for “the right time,” the right time is usually closer than people think.

A few things move MYGA annuity rates more than anything else:

- The term you pick, since five and seven-year terms often pay more than three-year ones

- How financially strong the carrier is

- Where overall interest rates are heading

Browse a Canvas Annuities MYGA listing and you’ll see rates lined up side by side from a dozen carriers, often with surprisingly different numbers for the exact same term length. That gap is the whole reason shopping matters instead of just grabbing whatever your bank counter person hands you.

What Are Fixed Indexed Annuities?

A fixed indexed annuity works on a different idea entirely. Your money’s growth gets tied to a market index, often the S&P 500, but your principal never actually touches the market. If the index drops, you don’t lose a dime. If it climbs, you get a slice of that climb, not the whole thing.

That’s the trade. Insurance companies cap your upside through participation rates and spread fees, which is their way of paying for the floor underneath you. Salespeople love calling these a high interest annuity or one of the high yield annuities on the market, and in a great year, the credited interest can genuinely beat a MYGA. In a flat year, though, it might credit you almost nothing. Neither outcome is guaranteed the way a MYGA’s number is.

MYGA vs Fixed Indexed Annuities: Key Differences

| Feature | MYGA | Fixed Indexed Annuity |

| Growth type | Fixed, guaranteed rate | Tied to a market index |

| Predictability | Very high | Variable, capped |

| Best for | Steady, guaranteed income | Growth potential with protection |

| Risk to principal | None within contract terms | None, but credited growth varies |

| Typical term | 3 to 7 years | Often 5 to 10 years |

A Real-World Scenario

Linda is 62. She had $150,000 parked in a savings account earning almost nothing, and she wasn’t about to gamble it on the market this close to retirement. She compared the best fixed annuity rates against a fixed indexed annuity quote for a couple of weeks, talked it over with her son, and landed on a five-year MYGA. Not because it was flashy. Because she wanted to know, down to the dollar, what her account would say in five years. It’s grown exactly as promised since. No surprises, which, at her stage of life, was the entire point.

Who Fits Which Annuity

A MYGA usually wins out for people who:

- Want guaranteed annuity rates and zero downside surprises

- Are within a few years of retirement and can’t stomach a market dip

- Would rather keep things simple than chase an extra percentage point

A fixed indexed annuity tends to make more sense if you:

- Have a longer runway before you’ll need the money

- Like the idea of some market-linked upside

- Are fine with caps in exchange for downside protection

How to Pick Between the Two

Get honest with yourself: do you want certainty, or are you okay trading some of it for growth potential? Pull multiple quotes. Best MYGA rates and FIA caps both swing by carrier, sometimes more than you’d expect. Read the surrender schedule before anything else. It matters more than the headline rate. Line the term up with when you’ll actually need the cash, not a random number that sounded good.

If your primary goal is converting your accumulated assets into reliable payouts, learning more about income annuities or setting up highly structured fixed income annuities can help bridge the gap. Always sit down with a licensed agent who can show you real multi year guaranteed annuity rates rather than a marketing flyer from last year.

Frequently Asked Questions

Is a MYGA worth it right now?

If guaranteed annuity rates without market exposure sound appealing, yes, particularly while MYGA rates today are still holding up well.

Can a fixed indexed annuity lose value?

Your principal can’t drop from market performance. What changes year to year is how much interest gets credited on top of it.

What does MYGA stand for?

Multi-Year Guaranteed Annuity. Three words that describe the entire product better than most marketing ever could.

What is a MYGA annuity exactly?

It’s a contract with an insurance company where you deposit a lump sum and get a fixed interest rate locked in for a set number of years, usually three to seven.

How do I find the best MYGA rates?

Compare quotes across multiple carriers rather than one. Rates for the same term can differ more than people expect, so a few minutes of comparison shopping can mean real money over the contract.

What’s the main difference between a MYGA and a fixed indexed annuity?

A MYGA gives you one fixed rate, guaranteed for the whole term. A fixed indexed annuity ties your growth to a market index with a cap, so your return can be higher or lower depending on the market that year. If you are looking for the absolute best annuity for retirement income to match your exact goals, it is crucial to analyze how these structures align with your timeline.

Is my money locked up with a MYGA?

Yes, for the contract term you choose. Pulling money out early usually triggers a surrender charge, so only commit funds you won’t need before the term ends.

Are multi year guaranteed annuity rates the same at every insurance company?

No. Rates vary by carrier, term length, and the company’s current financial strength rating, which is exactly why shopping around matters before signing anything.

Can I lose my principal in either a MYGA or a fixed indexed annuity?

No, both protect your principal from market losses. The difference is in how much, or how little, your money grows on top of it.

Final Thoughts

The MYGA vs fixed indexed annuities question doesn’t really have a universal winner. It has a winner for you, based on how close you are to retirement and how you feel about trading certainty for upside. A MYGA annuity suits the person who wants to stop thinking about it once the contract’s signed. A fixed indexed annuity suits someone willing to ride a little uncertainty for the chance at more.

Either way, this isn’t a decision to make off a Google search alone. Setting up structured guaranteed income plans requires analyzing how these fixed tax-deferred vehicles blend with your broader financial roadmap. Reach out to RGP Agency and talk through current rates on both sides with someone who’ll give you real numbers, not guesses.

Editorial Review & About the Authors

Written & Reviewed By: Pablo Pérez

This article was authored and technically reviewed by Pablo Pérez, senior financial advisor and co-founder of RGP Agency. Led by the husband-and-wife team of Pablo and Genesis Pérez, RGP Agency is a family-devoted, community-centric financial planning organization. Based in Texas, the Pérez family and their team of advocates specialize in crafting wealth preservation, annuity planning, guaranteed retirement income strategies, and legacy protection tailored to individual family dreams and business realities. To learn more about our mission, core values, and licensing, visit our official About Us page.

Corporate Headquarters & Contact Verification

For MYGA rate comparisons, fixed indexed annuity quotes, or to verify agent credentials, you can contact our registered Texas office directly:

- Office Address: 8376 Davis Blvd, Suite 246, North Richland Hills, TX 76182

- Direct Phone: (817) 973-5255

- Official Website: rgpagency.com

References & Authority Citations

RGP Agency Editorial Team (2026)

MYGA & Fixed Indexed Annuity Retirement Income Strategies. RGP Agency Financial Planning Series. rgpagency.com/income-annuities/myga-multi-year-guaranteed-annuity/

NAIC (2024)

Annuity Buyer’s Guide Fixed and Indexed Annuity Standards. National Association of Insurance Commissioners. naic.org

LIMRA (2024)

U.S. Annuity Sales & Market Trends Report. limra.com

IRS Publication 575 (2024)

Pension and Annuity Income Tax Treatment of Annuity Contracts. Internal Revenue Service. irs.gov/pub/irs-pdf/p575.pdf

Insured Retirement Institute (2024)

Fixed and Fixed Indexed Annuity Market Performance Standards. irionline.org

Canvas Annuities (2024)

Multi-Year Guaranteed Annuity Rate Listings & Carrier Comparisons. canvasannuities.com

Social Share

Life Insurance

Protect your family’s future.

Health Insurance

Stay healthy, stay protected.

Income Annuities

Turn savings into steady income.